.png)

Over the last twenty years, India has undergone a transformation that would have seemed improbable at the turn of the millennium. 99% of villages are connected by all-weather roads, utilities like electricity, water, and gas reliably reach distant hamlets, and a new backbone of digital infrastructure–embodied in Aadhaar and UPI–has made frictionless identity and payments a reality even for first-time internet users1. In parallel, financial inclusion has gained ground: microfinance, nimble NBFCs, and bespoke credit products, from two-wheeler loans to small-ticket housing and education finance, now reach corners of the country bankers historically wouldn’t touch. RBI's financial inclusion index has increased by over 50% since 2017.

The cumulative impact? India’s Entrepreneurial Households–farmers, shopkeepers, self-employed business owners–have become a ready and rapidly addressable market for essential services, spanning finance, healthcare, education, and agri-value chains.

Yet, less than a tenth of total venture capital and private equity funding in India reaches these Entrepreneurial Household-focused companies2. They remain structurally undercapitalized, often valued less generously, and unable to secure growth equity on the same magnitude as their urban-focused peers.

Why This Made Sense - Until Recently

For decades, this lack of capital flow was rooted in logic. Investors faced structural hurdles that made the rural market, where most Entrepreneurial Households reside, a slow, high-risk proposition.

- Asset-Heavy Scale: Every scale-up was asset-heavy, requiring significant physical investment in distribution and infrastructure.

- Missing Digital Rails: Digital rails were patchy or nonexistent, meaning every transaction was physical, and technology couldn't be leveraged for efficiency.

- Slow Returns: Financial returns materialized slowly, often falling outside of a typical VC/PE time horizon.

The Picture Has Shifted

Today, this old reasoning no longer holds; undercapitalization results from a perceptual, not structural gap. The massive “densification” of infrastructure, physical and digital, means that capital deployed today works at a pace and reach unimaginable two decades ago.

The proof is in the performance:

- Accelerated Financial Scale: Take NBFCs. Our research shows that twenty years ago, building a ₹1,000 crore loan book took 9.4 years on average. In the last decade, this time has been cut significantly, with modern firms taking just over 6 years to reach the same benchmark3. This faster scaling is powered by digital-first operations, strategic co-lending models, and a sharp focus on specialized products.

- Innovative "Phygital" Models: This innovation is not limited to finance. Consider rural healthcare startup CureBay, with their ‘e-clinic’ model. This is a business that straddles the best of both worlds: brick-and-mortar clinics and pharmacies on the ground, seamlessly coupled with telehealth connectivity that routes patients from remote villages to urban doctors in real time. This “phygital” model means essential services are both affordable and accessible–without the capital drag of building hundreds of traditional hospitals. For CureBay this has allowed them to deliver healthcare to over half a million customers in 5 years.

- Market-Beating Returns: Performance data bears this out. The EHI Index, tracking businesses serving Entrepreneurial Households, has outperformed both the Nifty 50 and Nifty Financial Services indices on revenue growth, while matching these blue-chips for profitability. These businesses are generating market-beating returns at real scale (the Index has a combined market cap of $160B)4.

The Capital Market Hasn’t Caught Up

What then explains the capital drought? It is certainly not the absence of addressable demand, nor a lack of proven models or technology rails. The answer lies within the world of capital.

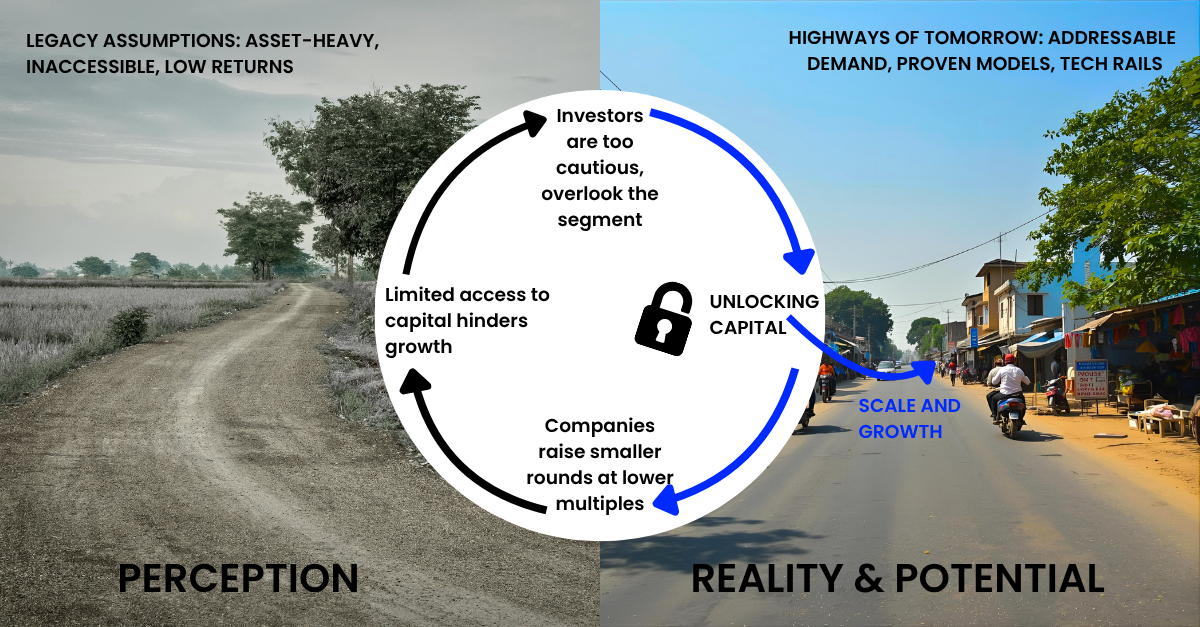

Too often, we benchmark these companies against legacy assumptions: asset-heavy distribution, inaccessible markets, and low returns. We are, in effect, using the rearview mirror to drive a vehicle engineered for the highways of tomorrow.

This creates a self-reinforcing cycle of undercapitalization:

- Investors, using old benchmarks, are too cautious and overlook the segment.

- High-potential companies find themselves raising smaller rounds at lower multiples.

- With inadequate access to capital, these companies struggle to reach scale, further hampering their ability to fundraise

They get trapped in a cycle of capital scarcity, not because of their fundamentals, but because of outdated perceptions.

It’s Time to Update the Model

It’s time to move past this narrative. If digital rails can bring the most remote household onto the formal financial grid in minutes, if healthcare can be delivered affordably at scale using tech-augmented networks, and if investment performance consistently beats bellwether indices, then our old models are overdue for revision.

The urgency now is for large capital allocators to bridge the funding gap. That means valuing companies on today’s performance and tomorrow’s potential, not decades-old benchmarks.

Businesses serving Entrepreneurial Households represent India’s next growth engine. It’s time for capital markets to reflect this reality.

1 Source: Niti Aayog, World Bank, and UIDAI

2 EPIC World Research using Tracxn data

3 With an inflation-adjusted ₹1,500-crore benchmark, modern NBFCs still scale 35% faster than older NBFCs did to ₹1,000 crore.